On 8 June 2025, the Interchange Fee Regulation (IFR) turned 10, offering a timely moment to reflect on the impact it has had over the past decade. The IFR was introduced to lower card acceptance costs for merchants and ultimately reduce consumer prices. As a market intervention, it was a significant step toward a more competitive EU payment landscape. However, ten years on, concerns remain regarding its limited effects for merchants and on payment costs across the EU.

Capping interchange fees

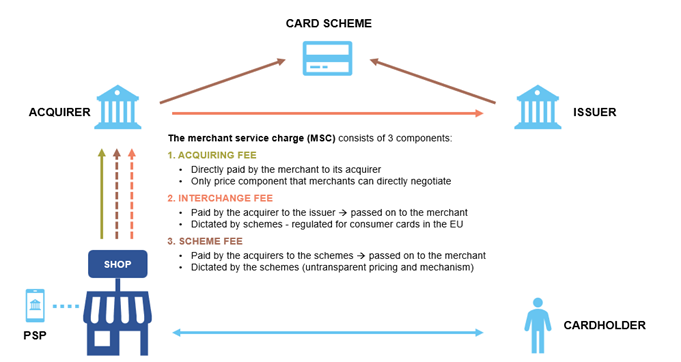

An interchange fee is a charge paid by a merchant’s bank (the acquirer) to the consumer’s bank (the issuer) each time a consumer makes a payment using a card. Although invisible to consumers, these fees are included within the Merchant Service Charge (MSC), the overall fee that merchants pay to their acquirer for accepting card payments. The MSC is composed of an (1) acquiring fee the (2) interchange fee, capped under the IFR, and the (3) scheme fee.

Prior to the IFR, interchange fees varied significantly across EU Member States. The higher the interchange fee was set, the more profitable a card would be for the issuer, which led to a phenomenon of reverse competition driving interchange fees up. Furthermore, merchants had no possibility of influencing the level of the fees which resulted in high and non-transparent costs. To address this, the IFR was introduced in 2015, to harmonise and reduce interchange fees across the EU by capping them at 0.2% for debit cards and 0.3% for consumer cards.

A Regulation challenged over the years

Ecommerce Europe has long stood for a European payments market without barriers, nor distinctions between local or cross-border, offline or online payments. In that regard, the IFR has been a significant step forward in the harmonisation of the internal market. However, the IFR had a temporary and limited impact on the overall cost of payments for merchants.

Rather than a price reduction, the caps led to a shift in the cost through a circumvention effect. While the interchange fee remained capped, other components of the MSC, and especially scheme fees imposed by international card schemes (ICS), increased to the extent that the reductions achieved by the IFR were surpassed. As a result, the average MSC applied by card schemes in the EU rose greatly in that period. This was notably underlined in a recent study commissioned by the European Commission, which showed that the average net MSC applied by card schemes in the EU almost doubled between 2018 and 2022, going from 0.27% to 0.44%[1]. 10 years later, the average cost of card payments in the EU has exceeded the levels observed at the time of the IFR’s implementation in 2015, neutralising the intended benefits of the Regulation[2].t

The rise of scheme fees does not reflect any specific cost drivers or additional risks and is uncorrelated with the rise in volume or value of transactions. Merchants believe that increasing the level of transparency in the payment value chain and shedding light on the practices, rules and fees applied by schemes is crucial.

Furthermore, adding to the issue of the increase in the cost of payments, a number of use cases that were left out of the IFR’s scope have become more and more burdensome for merchants. This is notably the case for cards issued outside the EU, but also meal vouchers and commercial cards. For the latter, its issuance has been on the rise, notably due to a practice of shifting cardholders from consumer to commercial cards, as those are not subject to the caps imposed by the IFR and thus more profitable for issuers and schemes.

Looking ahead, what’s next?

The Interchange Fee Regulation was well-intentioned, but it has not delivered on its core promise, with the average price of payments now higher than it was before its implementation. This is why Ecommerce Europe calls for a reopening of the IFR to address its limitations. It is time to take a more holistic approach that truly reduces costs, promotes competition and fairness, but also supports the European digital economy. We believe that this could be achieved through:

- Expanding the scope of the IFR to include scheme fees to ensure true competitive pricing.

- Addressing the remaining IFR exemptions that were left out of the scope, such as commercial cards, meal vouchers, and inter-regional payments.

- Increasing the transparency and information obligations within the IFR, notably with consultation and better information on updated scheme rules and fees.

- Harmonising supervision and increasing the EU’s oversight over the EU payment market, and especially on price evolution and ICS’s practices.

If you want to learn more about the IFR, and the broader issue of the cost of payments, you can read Ecommerce Europe’s full position paper here.

[1] https://competition-policy.ec.europa.eu/document/65d4f65a-6b23-49c7-91cb-e5cd166a19ed_en

[2]https://www.eurocommerce.eu/2020/12/benefit-of-interchange-fee-regulation-now-nullified-by-fee-increases/